PACE: A Financing Tool For Green Energy Improvements

PACE is a financing tool which has a green halo around it. Its purpose is to promote energy efficiency and the use of renewable energy. PACE, an acronym for Property Assessed Clean Energy, was passed by the Nebraska Unicameral in 2016. By comparison, it has existed in California since 2007.

Owners and property developers of course are already able to finance these types of improvements, but this gives them a tool so that the loan term is longer (as much as 25 years) since the loan is repaid through a voluntary “tax” assessment on the improved property that runs with the land. This super-priority of the lien allows for a lower interest rate. This allows borrowers to finance improvements that ordinarily would not be economical. To date, over $60 million has been lent pursuant to PACE loans in Omaha. Nationwide, over $1.5 billion of commercial PACE loans have been made to date.

The identity of the lenders making these type of loans is what is really interesting. Until May of this year, none of these loans were made by a bank. The first bank loan for an Omaha PACE project occurred in May of this year. For the first five years of PACE loans in Omaha, all of the PACE loans were made by non-bank, PACE-specialty lenders. I handled first bank PACE loan in Omaha in May.

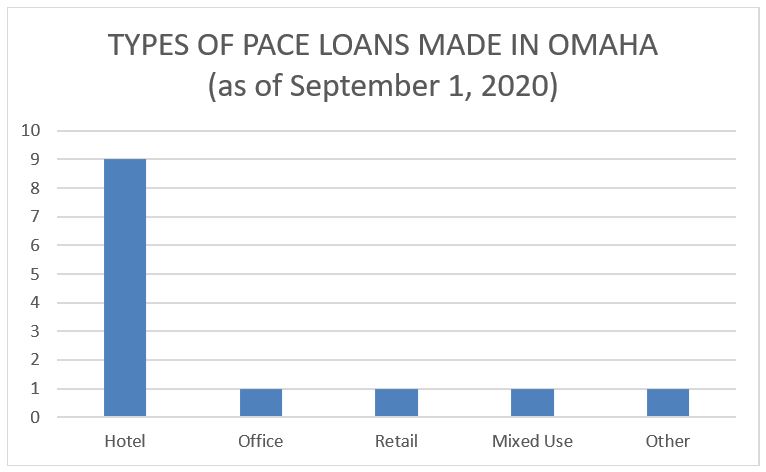

The purpose of those loans in Omaha is also revealing. Figure 1 is a chart that shows the type of PACE loans that have already been made in Omaha. As you can see, this is very heavily weighted in favor of hotels. PACE loans work well for hotels because the hotel can “pass through” the PACE special assessment to a guest on top of the actual hotel bill. When making a hotel reservation, the PACE special assessment (as well as sales tax) is not included in the suggested rate. But when it comes time to check out, the customer gets the bill.

FIGURE 1

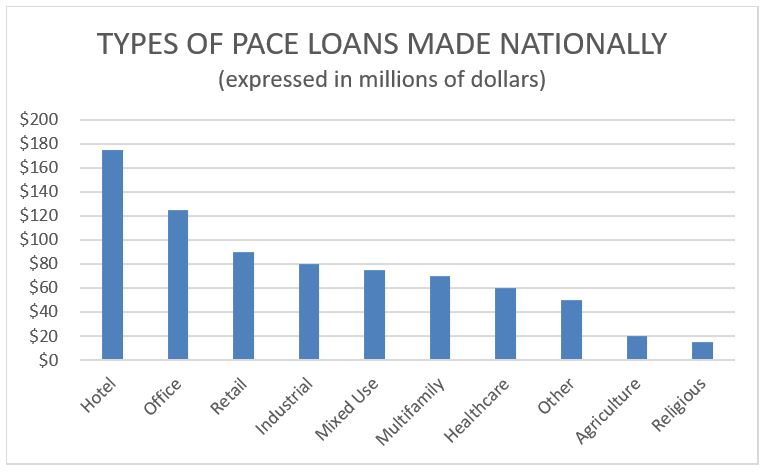

Figure 2 shows the distribution of commercial PACE loans nationwide. This indicates other types of commercial PACE loans not currently done in Nebraska. You will notice that it is not so heavily weighted in favor of hotels.

FIGURE 2

Two other types of borrowers seem really ripe for this type of loan. The first is a landlord that wants to do this type of energy savings work. The payments on the loan are in effect payment of special assessments or real estate taxes that can be “passed through” to the tenant. The tenant then pays all taxes, or in this case special assessments, levied against the leased property. So far, only two of these types of borrowers show up on Figure 1.

The second is a non-profit entity, like a church, which is having difficulty finding typical real estate financing. Commercial construction loans typically have a 3-5 year maturity period, making the repayment terms difficult when it comes to energy savings projects. PACE changes all of this by allowing the non-profit to finance energy efficiency projects through a special assessment levied by the local government. Since the loan has a super-priority and the county will enforce this assessment just like any other delinquent tax obligation, lenders feel secure in providing loans with terms of up to 25 years. This results in a positive cash flow for the non-profit since the monthly savings generated by the energy project are greater than the loan repayment obligation. However, unlike national PACE loans shown in Figure 2, no Omaha PACE loans have been made to date for churches or other non-profits.

The definition of improvements that can be made with a PACE loan is very broadly written. They would include any acquisition, installation or modification benefiting property that is designed to reduce the utility demand or consumption in existing buildings or new construction.

A PACE loan can finance the costs of materials and labor, and can also finance the costs for permit fees, inspection fees, application and administrative fees, bank fees and other fees incurred by the owner/borrower for the installation of the project.

Earlier I mentioned that these loans could have long payment terms beneficial to borrowers. The term of the annual assessments (loan payments) for repaying the loan may not exceed the “weighted average useful life” of the energy project. The calculation of the weighted average useful life would follow this simple example: Say there are two separate energy reduction projects being installed, each with different useful lives. This includes a chiller with a 30-year useful life and LED lighting with a 20-year useful life. Assume that both the chiller and the lights cost the same. Then the “weighted average useful life”, or the term of the loan, would be the average useful life of the two separate projects. That is: (30+20) ÷ 2 = 25 years.

PACE loans represent a new capital stack for borrowers, whether they are commercial borrowers or nonprofits. This also represents a new group of borrowers that have not been served by banks in Nebraska.

Related Attorneys