Minimizing Taxes In Designing The Sale Of A Business

When Sam came to see us, he was very excited about the opportunity to sell his business to a private equity group named PEG. However, Sam was stunned by the initial tax projections we provided him shortly after he engaged us. At the price he was hoping to receive, he was looking at a double federal tax on the sale (i.e., a tax upon his “C” corporation as well as a tax when the proceeds were distributed to him). He was also looking at a double state tax, since he lived in Nebraska which taxes both the sale and distribution of the sale proceeds. Sam wanted to know what his options were.

In the Next Move For Business Owners Program I have identified and addressed the top 12 principal reasons which cause owner transitions and exits to be unsuccessful. Each of these impacts the company’s ongoing annual profitability as well as an owner’s transition and future exit results. This article addresses the 10th of these 12 reasons:

Reason #10. Missing Pre-Exit Tax Tools. Pre-Exit tax minimization steps haven’t been taken in time or at all.

Most business owners realize that a sale of their business will typically result in federal and state income tax obligations which will be created and due upon the sale of a business. Depending on the (a) business structure, (b) terms of the sale, (c) the location of the seller, and (d) pre-exit planning by the seller, these income taxes will either be maximized or minimized.

Business owners and buyers have a number of alternatives for designing the transfer of a business. The choice of structure depends on several factors, including the parties’ objectives and relative negotiating leverage, the seller’s present corporate structure and tax attributes, and the nature of the buyer.

This article reviews selected alternatives that Sam, with the proper pre-exit and transaction planning, could have considered:

Sam’s Facts

| Sam provided us with the following facts: | |

| • Business Value: | $10 Million |

| • Stock Basis: | $2 Million |

| • Asset Basis: | $2 Million |

| We made the following assumptions: | |

| • Tax Rates: | |

| – Corporate and Personal Ordinary: 40% (35% Federal; 5% State) | |

| – Personal Capital Gain & Dividends: 20% (15% Federal; 5% State) | |

Base Case

Double Taxed Asset Sale. Sam operated his business in a “C” corporation named SamCo. PEG told Sam it wanted to buy the assets of his “C” corporation (which would then distribute the sale proceeds to him). Both SamCo and Sam (as its shareholder) would be taxed on the gain. Tax Cost = $4.2M.

Permanent Tax Saving Alternatives

The following are some of the alternatives we discussed with Sam regarding his possible sale to PEG or to other potential future buyers.

Recent “S” Election Asset Sale. The buyer purchases the assets of your “S” corporation which within 10 years of sale was a “C” corporation. Your “S” corporation will be taxed on the “built in gain” that existed at the time of the “S” election and you as the shareholder will be taxed when the (after tax) sale proceeds are distributed. Tax Cost = $2.9M.

Single Taxed Asset Sale (Unfavorable Price Allocation). The buyer purchases the assets of your “S” corporation which has been an “S” corporation since its inception or for at least 10 years. You as the shareholder are taxed once on the gain. However, the terms allocate a high proportion to ordinary income assets (such as inventory, receivables and depreciated tangible property), resulting in significant ordinary income gain. Tax Cost = $2.6M.

Single Taxed Asset Sale (Favorable Price Allocation). This transaction is identical to the preceding example, however the parties allocate a larger percentage to capital gain assets (such as goodwill, going concern value and tangible property with little ordinary recapture). With the higher proportion allocated to capital gain assets, the overall tax is reduced to the seller. Tax Cost = $1.8M.

Single Taxed “C” Stock Sale. The buyer purchases the stock of your “C” corporation. You are taxed on the gain, but the buyer doesn’t receive a tax basis step-up in the company assets (which usually results in a lower negotiated price) and most buyers do not want to buy stock due to the risk of inheriting unknown liabilities. Tax Cost = $1.6M.

“C” Stock Sale (With No State Tax). The seller can avoid state tax on the gain by residing in a state that doesn’t have an income tax or by meeting an exemption. If the seller resides in a taxable state but intends to move to a no tax state, certain actions to demonstrate the change in residency must occur before the sale. In Nebraska, sellers can meet an exemption if the corporation has at least 5 shareholders and at least 10% is owned by owner(s) not related to the other 90%. Again, however, a well advised buyer will demand a lower purchase price in the case of a stock sale. Tax Cost = $1.2M.

“S” Stock Sale (With Basis Bump). The buyer purchases the stock of your “S” corporation. You are taxed on the gain, but the taxable gain may be significantly less where you have been a profitable “S” corporation, since time builds tax-reducing stock basis. It is likely that a buyer of stock in an “S” corporation will want a 338(h)(10) election to receive a basis step-up. Tax Cost = $1.0M.

ESOP Stock Sale (With ESOP Note). You sell your “C” corporation stock to an Employee Stock Ownership Plan (which after the sale owns at least 30% of the stock). This can defer the tax on the stock sold to the ESOP for as long as you invest the proceeds in qualified securities. This can include an ESOP Note, which allows for a managed account where securities can be sold and reinvested without triggering the deferred gain. If you hold the Note until death, your estate receives a stepped up basis, and thus a permanent tax savings. Tax Cost = $-0-

Tax Deferral Alternatives

We also told Sam about some tax deferral techniques that could be used.

Tax Deferred Stock Exchange. The buyer purchases the stock or assets of your corporation in exchange for stock of the buyer’s corporation in a transaction that qualifies as tax free under the Internal Revenue Code. Tax on your gain is deferred until you sell the buyer’s stock.

Tax Deferred Installment Sale. The buyer purchases your stock or the assets of your corporation in exchange for an installment promissory note payable to you over time. This can defer some or all of the tax on the transaction until payments are received.

Tax Deferred Sale To ESOP. This is the same as the ESOP transaction, but you don’t use the ESOP Note. If the replacement securities are sold, the deferred gain becomes taxable.

Partial Equity Rollover

Sam told us that he and PEG had discussed the possibility of Sam retaining some ownership and he wanted to know if he would be taxed on the retained portion. Here Sam would retain partial equity in his business by receiving a portion of the ownership (e.g. 20%) in the entity which is set up by PEG to be the buyer. To avoid capital gain taxation on the retained equity, an “LLC Drop-Down” or an “S Corporation Inversion” transaction would need to be utilized.

The LLC Drop-Down Transaction. Private equity groups like PEG often encourage – and sellers often want – to leave part of their target company (“T”) stock in the deal. Sellers want this to be a tax-deferred rollover, i.e. they want no tax on their retained shares until they are sold in the future. The PEGs want to step-up the basis in T’s assets to the amount of the transaction price. This allows for higher future depreciation and amortization tax deductions.

The tax reality is that structures that allow sellers a tax-deferred rollover are generally not consistent with the basis step-up. An asset purchase is the best way for PEG to obtain a basis step-up. However, this results in 100% of the gain taxed (once if Target is an “S” corp.; twice if Target is a “C” corp.) even if part of the cash is reinvested by seller into the buyer.

How about doing a stock sale? One way for sellers to defer tax on a rollover is to do a stock sale (instead of an asset sale). No tax would be due on the retained stock. However, PEG doesn’t receive a basis step-up.

Can a 338(h)(10) election be used? This treats the stock sale as an asset sale for tax purposes. And it gives PEG a basis step-up. T must be an S Corporation and PEG must form an acquisition corporation to buy at least 80% of T stock. However, this doesn’t give the seller a tax deferred rollover. The sellers must pay tax on their pro rata portion of the taxable gain from the deemed asset sale.

There are some other problems with making a 338(h)(10) election. PEG cannot hold its T stock ownership in a partnership or LLC (a common private equity group approach). In addition, leveraged purchases (another common private equity group approach) can affect the 80% requirement and void the 338(h)(10).

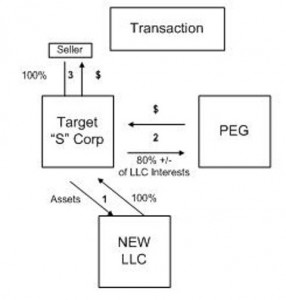

The “LLC Drop-Down” is a solution. A growing number of PEGs are buying companies using an LLC. This enables them to distribute debt refinancing proceeds and to sell the company without double tax. The LLC structure is also one of the few ways to do both a tax-deferred rollover with a basis step-up. (Besides its place in a partial equity rollover transaction, the “LLC Drop-Down” also provides a solution for a number of business owners’ estate planning, asset protection planning and transition planning objectives.)

This is how it’s done:

1. Target’s business is transferred to a new LLC.

2. PEG buys the desired percentage of the LLC from Target.

3. Target distributes the cash to its shareholders.

The tax results are as follows. This is treated as an asset purchase for the PEG (as a purchase of an undivided interest in T’s assets). No taxable gain occurs on the retained seller’s share of the LLC business.

The end result of this transaction is that the PEG owns 80% of the new LLC, while the seller retains 20% ownership of the new LLC through the Target “S” corporation.

This can be illustrated as follows:

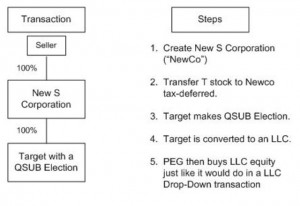

The “S Corporation Inversion” Transaction. This alternative can be attractive if a transfer of some of T’s assets is problematic. For example, due to restrictions or legal issues, various contracts, licenses, or intellectual property might not be readily transferable.

The seller and buyer can achieve the same tax results as the “LLC Drop Down” through an “S Corporation Inversion” transaction.

This is how it’s done:

Summary

These exit structure alternatives illustrate only some of the options available for designing a sale of a business. Other more involved alternatives, as well as tax efficient choices within each alternative, also exist, which can be addressed in the pre-exit and transaction planning process. Each proposed sale of a business provides its own set of business, financial and tax planning opportunities.

If you would like to discuss any of these strategies,please contact us. To see a powerpoint illustrating further details of each structure, advisors can visit the Advisor page at www.OwnersNextMove.com.

Related Attorneys